Contact

Contact How to shop

How to shopDelivery

Shopping guide

English

English

231 b

231 b

Delivery to Austria

Delivery to Austria

30-day return policy

Customers also purchased

/

/

Calendar

Calendar

31.99

€

31.99

€

/

/

Paperback

30.19

€

Paperback

30.19

€

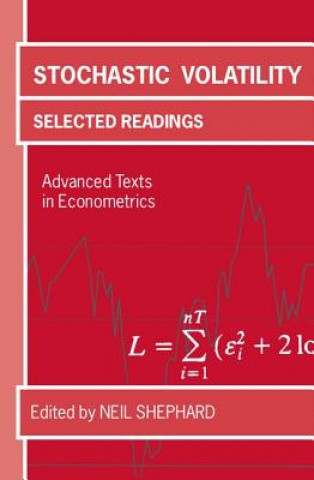

Stochastic volatility is the main concept used in the fields of financial economics and mathematical finance to deal with time-varying volatility in financial markets. This book brings together some of the main papers that have influenced the field of the econometrics of stochastic volatility, and shows that the development of this subject has been highly multidisciplinary, with results drawn from financial economics, probability theory, and econometrics, blending to produce methods and models that have aided our understanding of the realistic pricing of options, efficient asset allocation, and accurate risk assessment. A lengthy introduction by the editor connects the papers with the literature.

About the book

English

Categories

Give this book today

It's easy

1 Add to cart and choose Deliver as present at the checkout 2 We'll send you a voucher 3 The book will arrive at the recipient's addressYou might also be interested in

/

Hardback

48.49

€

/

Hardback

48.49

€

/

Paperback

21.49

€

/

Paperback

21.49

€

/

Paperback

8.89

€

/

Paperback

8.89

€

/

Paperback

37.49

€

/

Paperback

37.49

€

/

Hardback

15.39

€

/

Hardback

15.39

€

Hi! I'm Libroamiko, your book advisor.

How can I help you?